Investor Relations

Management Discussion and Analysis

BUSINESS REVIEW

The Group recorded an attributable loss of HK$19.0 million for the year ended March 31, 2019 (�FY2019�) compared to an attributable profit of HK$112.0 million for the year ended March 31, 2018 (�FY2018�) partly due to an exchange loss of HK$30.7 million in FY2019 as compared to an exchange gain of HK$33.4 million in FY2018. Excluding the exchange difference, the attributable profit of the core business would have been HK$11.7 million in FY2019 as compared to HK$78.6 million in FY2018. The decrease in attributable profit of the core business was mainly due to a decrease in revenue, which led to a decrease in gross profit in FY2019.

Revenue

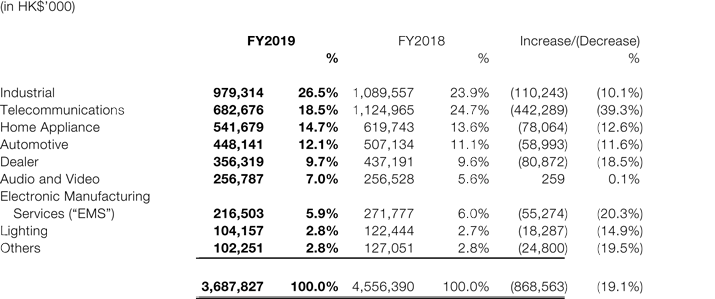

The Group's sales revenue had decreased by 19.1% year-on-year (�YOY�) from HK$4,556.4 million in FY2018 to HK$3,687.8 million in FY2019.

FY2019 was one of the toughest and most challenging year for the businesses worldwide, with many macro developments that led to global uncertainty. Although it had started well following the positive economic growth and strong demand in FY2018, the escalating of US-China trade tensions had resulted in weak consumer and business sentiments and greatly impacted market confidence over the course of the year. In response to this, customers and manufacturers held back aggressive development and expansion plans, tightened control on purchases and trimmed down inventory levels. In addition, the depreciation of Renminbi (�RMB�) further reduced the buying power of domestic customers in China. The outcome was a drastic decline in demand in both the export and the Chinese domestic market for electronic componentry.

The impact was felt across the whole market and not to a specific application segment. In line with this, the revenue generated by all (except one of) our business segments declined in FY2019; we sustained a smaller decline in sales in our Industrial, Home Appliance and Automotive segments because of our ongoing efforts in developing the value-added services in these applications.

Turnover by Market Segment Analysis

Industrial

The Industrial segment recorded revenue of HK$979.3 million in FY2019, a drop of 10.1% as compared to FY2018. The business was affected by the current US-China trade tensions. However, we are optimistically confident of this segment's potential in the long term due to the rapid growth and rising trend towards industrialization, factory automation and energy saving improvements. In line with this, the Group has committed extensive resources in this segment to position itself for future opportunities.

Telecommunications

The Telecommunications segment was the Group's second largest revenue generator in FY2019 contributing sales of HK$682.7 million. There was a significant YOY drop of 39.3% as compared to FY2018 due to the negative combination of US-China trade tensions as well as the migration from the 4G to 5G market. The mature and saturated smartphone market is very much dependent on the intentions of consumers to replace their mobile phones. Under the current conditions, most have adopted a wait-and-see attitude, which had affected demand in this segment. The Group will put more focus to improve the operational efficiency in this segment to better monitor the supply chain in order to avoid any potential risk on the inventory.

Home Appliance

Revenue from the Home Appliance segment was HK$541.7 million in FY2019, representing a decrease of 12.6% as compared to FY2018. This segment started well in FY2019 with strong domestic demand but it eventually succumbed to worsening market sentiments with manufacturers trimming down inventory and pushing out orders to keep a lower risk position. In response to this situation, we reduced our purchases and maintained a reasonable inventory level.

We remain positive about the long term prospects of this segment and will continue to develop more solutions that cater to higher energy efficiency and smart features for the products.

Automotive

Revenue from the Automotive segment decreased by 11.6% to HK$448.1 million in FY2019 as compared to FY2018. The domestic demand and our effort to launch new designs enabled us to sustain the business in the first half of FY2019. However, the second half was affected by the same issues of US-China trade tensions and poor consumer sentiments in China, which resulted in a significant fall in both export and domestic demand. We put more effort to manage the supply chain to avoid unexpected risk in both cash flow and inventory in this market.

The Group's commitment in this segment is still strong and we will continue to invest resources to develop more solutions and value-added services in this market to ride on the trend of electrification and digitalization.

Dealer

The revenue from this segment was HK$356.3 million in FY2019, a 18.5% drop as compared to FY2018. This segment has traditionally been the fastest to react to market changes. With the current conditions, the dealers have become cautious and stopped stocking up on inventory and participating in sales programmes. The rapid depreciation in RMB had also further damaged the business in this segment.

Audio and Video

Revenue from the Audio and Video segment was HK$256.8 million in FY2019, a marginal YOY increase of 0.1% as compared to FY2018. This segment was greatly impacted by the US-China trade tensions, particularly demand for traditional audio and video products. The decline in sales was partially offset by sustained demand for high-end and portable products and supported by the project we secured in 2018 for the European market for the period until the end of FY2019.

We believe that this segment remains unstable and we will carefully monitor the progress of each project and our inventory levels to protect against any potential risk.

EMS

This segment recorded a 20.3% decrease in revenue in FY2019 as compared to FY2018 to HK$216.5 million. The uncertain macro environment resulted in cancelled orders from customers. We will be more nimble in responding to and anticipating changes in orders and the buffer inventory levels to avoid the obsolete stock pile-up.

Lighting

Revenue from this segment was HK$104.2 million in FY2019, a drop of 14.9% as compared to FY2018. During the year, demand remained weak, which was compounded by a worsening export market in the second half of FY2019. However, the positive trend in an otherwise gloomy environment is that manufacturers are putting more focus on developing smart lighting in the Internet of Things market. This becomes a new trend and is good for us to develop more solutions in this segment.

Others

The applications in this segment include Toys, Health Care and Security, which were affected by the weak consumer confidence and hence the demand is unstable. Revenue from this segment dropped 19.5% in FY2019 as compared to FY2018 to HK$102.3 million.

Gross Profit Margin

The Group's gross profit margin slightly increased from 8.7% in FY2018 to 8.9% in FY2019. This was attributed to the Group's investment in engineering resources and sales network to provide value-added services to customers in our key focus segments, such as Automotive, Industrial and Home Appliance, which led to better returns. Thus the Group's profit margin maintained at a similar level as last year.

Distribution Costs

Distribution costs decreased by HK$17.3 million, or 28.7%, from HK$60.4 million in FY2018 to HK$43.1 million in FY2019. The decrease was mainly due to lower sales incentive expense, which was in line with the decrease in sales revenue.

Administrative Expenses

Administrative expenses increased by HK$8.6 million, or 4.0%, from HK$211.5 million in FY2018 to HK$220.1 million in FY2019. This was mainly due to an increase in premises and warehouse removal expenses resulting from extra rental expenses incurred for the new warehouse in Hong Kong for renovation and removal in the current year.

Other Gains and Losses

Other losses of HK$31.3 million in FY2019 included an exchange loss of HK$30.7 million, mainly arising from the depreciation of RMB. Other gains of HK$33.7 million in FY2018 included an exchange gain of HK$33.4 million, mainly arising from the appreciation of the RMB.

Impairment Losses, Net of Reversal

Impairment losses of HK$8.8 million in FY2019 and reversal of impairment losses of HK$4.1 million in FY2018 represented the impairment losses/reversal of impairment losses on trade receivables.

Finance Costs

Finance costs increased by HK$15.7 million, or 50.9%, from HK$30.9 million in FY2018 to HK$46.6 million in FY2019. This was mainly attributable to an increase in average trust receipt loans and the higher average interest rate during the year. As at March 31, 2019, the interest rate of trust receipt loans was ranging from 2.98% to 5.06% (March 31, 2018: 2.11% to 3.75%) per annum.

LIQUIDITY AND FINANCIAL RESOURCES

Financial Position

As compared to the previous financial year ended March 31, 2018, trust receipt loans decreased by HK$226.4 million. Trade payables decreased from HK$397.5 million as at March 31, 2018 to HK$310.9 million as at March 31, 2019. The decrease in trust receipt loans was mainly due to the decrease in purchases towards the end of the year under review. Trade receivables as at March 31, 2019 decreased by HK$187.5 million when compared to those as at March 31, 2018, due to a decrease in sales revenue towards the end of the year under review, and the debtors turnover days slightly decreased from 2.6 months to 2.5 months.

As at March 31, 2019, the Group's current ratio (current assets/current liabilities) was 1.29 (March 31, 2018: 1.31).

Inventories

Inventories slightly decreased from HK$691.0 million as at March 31, 2018 to HK$689.9 million as at March 31, 2019. The inventory turnover days increased from 1.7 months to 2.5 months.

Cash Flow

As at March 31, 2019, the Group had a working capital of HK$398.9 million, which included a cash balance of HK$297.5 million, compared to a working capital of HK$470.9 million, which included a cash balance of HK$327.1 million as at March 31, 2018. The decrease in cash by HK$29.6 million was primarily attributable to the net effect of cash outflows of HK$29.1 million in investing activities and HK$50.7 million in financing activities and inflow of HK$54.4 million generated from operating activities. The Group's cash balance was mainly denominated in United States dollars (�USD�), RMB and Hong Kong dollars (�HKD�).

Cash inflow generated from operating activities was mainly attributable to the net effect of a decrease in trade receivables due to decreased sales revenue towards the end of the year under review but partially offset by a decrease in trade payables.

Cash outflow in financing activities was mainly attributable to the overall decreases in trust receipt loans and bank borrowings as a result of the decrease in purchases.

Borrowings and Banking Facilities

As at March 31, 2019, fixed-rate bank borrowings of HK$225.0 million (March 31, 2018: HK$170.0 million) were unsecured and repayable in quarterly or half-yearly installments ending in the financial year of 2020. The fixed-rate bank borrowings were denominated in HKD.

Unsecured fixed-rate bank borrowings bore interest at a weighted average effective rate of 4.62% per annum while variable-rate bank borrowings bore interest at a weighted average effective rate of 3.83% per annum as at March 31, 2019. The variable-rate bank borrowings were denominated in USD and HKD.

As at March 31, 2019, trust receipt loans were unsecured and repayable within one year and bore interest rates ranged from 2.98% to 5.06% per annum. As at March 31, 2019, the Group had unutilised banking facilities of HK$701.8 million (March 31, 2018: HK$457.6 million).

The aggregate amount of the Group's borrowings and debt securities were as follows:

Amount repayable in one year or less, or on demand

Amount repayable after one year

As at March 31, 2019, the Group's trade receivables amounted to HK$192.1 million (March 31, 2018: HK$76.5 million), which were transferred to banks by discounting those trade receivables on a full recourse basis. As the Group had not transferred the significant risks and rewards relating to these receivables, it continued to recognise the full carrying amount of the receivables and had recognised the cash received on the transfer as a secured borrowing amounting to HK$173.5 million (March 31, 2018: HK$61.3 million).

Foreign Exchange Risk Management

The Group operates in Hong Kong, the People's Republic of China (�PRC�) and Taiwan. It incurred foreign currency risk mainly on sales and purchases that were denominated in currencies other than its functional currencies. Sales are mainly denominated in USD, RMB, HKD and Taiwan dollars (�TWD�) whereas purchases are mainly denominated in USD, Japanese yen (�JPY�), RMB and HKD. Therefore, the exposure in exchange rate risks mainly arises from fluctuations in foreign currencies against the functional currencies. Given the pegged exchange rate between HKD and USD, the exposure of entities that use HKD as their respective functional currency to the fluctuations in USD is minimal. However, exchange rate fluctuations between RMB and USD, RMB and JPY, HKD and JPY, or TWD and USD could affect the Group's performance and asset value. The Group has a foreign currency hedging policy to monitor and maintain its foreign exchange exposure at an acceptable level.

Net Gearing Ratio

The net gearing ratio as at March 31, 2019 was 108.1% (March 31, 2018: 101.9%). The net gearing ratio was derived by dividing net debts (representing interest-bearing bank borrowings, trust receipt loans and bills payables minus cash and cash equivalents and restricted bank deposits) by shareholders' equity at the end of a given period. The increase was mainly due to a decrease in shareholders' equity from HK$716.1 million to HK$670.6 million.

Contingent Liabilities

The Company had given corporate guarantees (unsecured) to its banks in respect of banking facilities granted to its subsidiaries. As at March 31, 2019, the aggregate banking facilities granted to the subsidiaries were HK$1,555.3 million (March 31, 2018: HK$1,455.8 million), of which HK$859.3 million (March 31, 2018: HK$1,002.1 million) was utilised and guaranteed by the Company.

As at March 31, 2019, the Company had also given guarantees to a supplier in relation to the subsidiaries' settlement of the respective payables. The aggregate amount payable to this supplier under guarantee was HK$249.4 million (March 31, 2018: HK$365.5 million).

STRATEGY AND PROSPECTS

The ongoing US-China trade tensions and the resulting implementation of tariffs are a threat to China's economy, and are expected to dent US growth. With no near-term resolution in sight, a prolonged dispute will certainly worsen the global economy.

Given its track record of more than 30 years, the Group remains confident of its ability to weather the current market conditions as it focuses its efforts and resources on the key growth segments it has identified, namely Automotive, Industrial and Home Appliance.

In view of the considerable downside risks and certain headwinds in the macro-environment, the Group has, during the year, taken several measures in facing this challenging situation, including tightening its cost and expenses control, mitigating the credit risk of debtors and kept our inventory at appropriate levels. The Group will continue to be prudent in managing its operations and sustaining a healthy liquidity position in order to support the long-term growth.

EMPLOYEES AND REMUNERATION POLICIES

As at March 31, 2019, the Group had a workforce of 467 (March 31, 2018: 454) full-time employees, of which 32.8% worked in Hong Kong, 63.8% in the PRC and the remainder in Taiwan.

The Group actively pursues a strategy of recruiting, retaining and developing talented employees by (i) providing them with regular training programmes to ensure that they are kept abreast of the latest information pertaining to the products distributed by the Group, technological developments and market conditions of the electronics industry; (ii) aligning employees' compensation and incentives with their performance; and (iii) providing them with a clear career path with opportunities for taking on additional responsibilities and securing promotions. Besides, the Company has adopted employee share option schemes to reward the eligible employees for their contribution to the Group.

While the Group's employees in Hong Kong and Taiwan are required to participate in the mandatory provident fund scheme and a defined contribution pension scheme respectively, the Group makes contributions to various government-sponsored employee-benefit funds, including social insurance fund, housing fund, basic pension insurance fund and unemployment, maternity and work-related insurance funds for its employees in the PRC in accordance with the applicable PRC laws and regulations.

Further, the remuneration committee of the board of directors of the Company (the �Board�) reviews and recommends to the Board the remuneration and compensation packages of the directors of the Company and senior management of the Group by reference to the salaries paid by comparable companies, their time commitment and responsibilities and the performance of the Group.

Focus on us

WeChat Public Number

Browse mobile terminal

Copyright©2024 Willas-Array Electronics (Group) Co., Ltd. All rights reserved

Technical Support:China Enterprise Power Kunshan SEO